Disclaimer: Views, opinions and analysis provided by guest speakers and participants are their own. Reproducing them on our website does not imply that they are endorsed by Neyen.

Setting the scene

Sarfina Adani, Consultant at Neyen started the workshop with a setting-scene presentation on the overview of blue carbon.

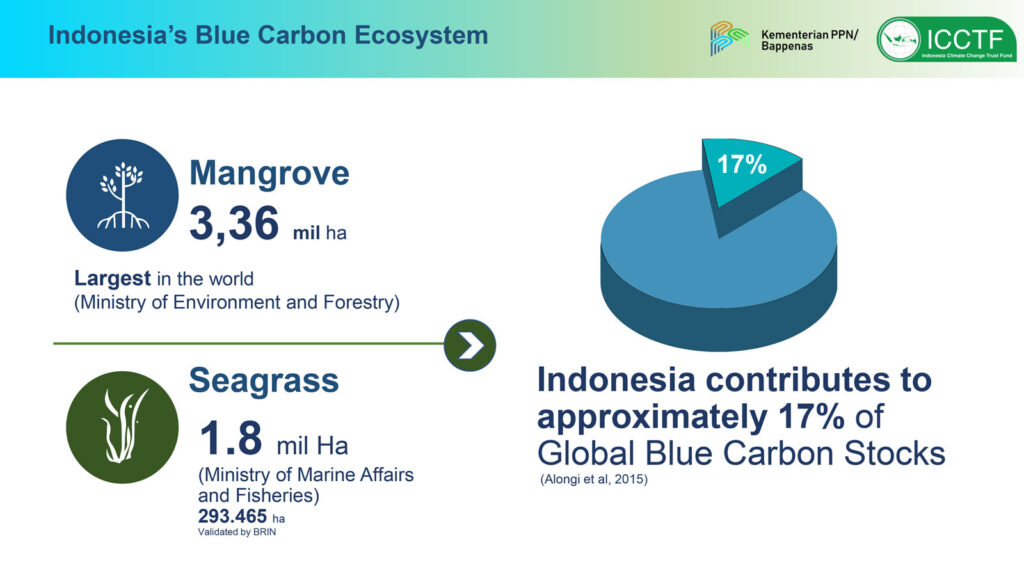

As an archipelagic country, Indonesia contributes approximately 17% of Global Blue Carbon Stocks. Based on the data from the Ministry of Environment and Forestry, Indonesia reserves up to 3.36 million ha of mangrove restoration, being the largest in the world. Mangroves also have the potential to absorb carbon emissions up to 11 mtCO2 per year in Indonesia. Indonesia then includes the concept of a “Blue Economy”, which may include blue carbon, as part of the economic transformation in achieving the 2045 Golden Indonesia vision.

Blue Carbon refers to carbon dioxide stored in coastal and marine ecosystems, such as mangroves, salt marshes, and seagrasses. Blue carbon plays an important role in both mitigation and adaptation measures for climate change. Due to its huge storage capacity, with a 3-7 times higher potential for sequestration compared to terrestrial forests, coastal ecosystems offer huge opportunities for mitigation activities. Other benefits like protection from flooding and local community empowerment are valuable for adaptation measures and become reasons why blue carbon activities need to be taken seriously.

Opportunities and challenges of blue carbon implementation in West Java

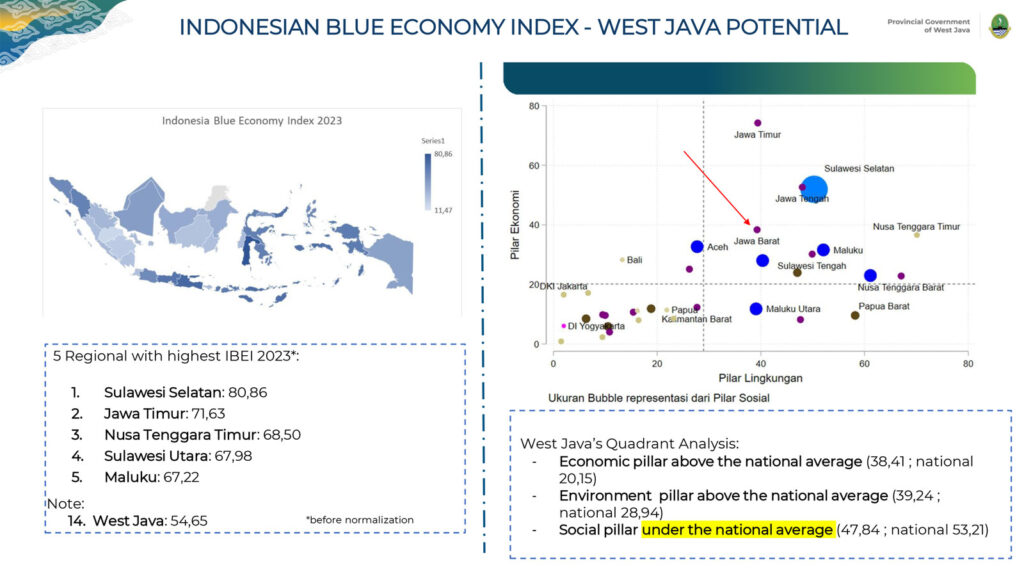

Guest speaker Eka Jatnika Sundana, Head of Economy & Natural Resources Division of Regional Development Planning Agency of West Java Province (Bappeda Jabar) showcased opportunities and challenges of blue carbon implementation in several areas in West Java. West Java is known to have potential in blue carbon and with a high production level of aquaculture it is the nation’s second-largest. However, data from Bappeda Jabar shows that the average contribution of the Blue Economy sector to West Java’s Regional GDP in the last 5 years is still low, around only 2% which mainly contributed to the fisheries sector. This is likely due to other development challenges in West Java that become the government’s priorities, such as extreme poverty and stunting.

The need for scalable top-down frameworks

Eka also added that the operational definition of “blue economy” is still limited to conventional sectors (capture fisheries, aquaculture, and fish processing). Moreover, The Indonesia Blue Economy Index (IBEI), which was developed by Bappenas for Indonesian regions’ blue economy implementation, does not yet capture a clear standardized scoring method (e.g., using “good quality” for indicators). This means that regions like West Java will only be able to maximize their blue carbon potential and exercise a blue economy (bottom-up) when the Indonesian central government ensures that frameworks are designed with scalability and applicability (top-down).

Four main challenges for Indonesian blue carbon ecosystems

During the discussion Amrullah Rosadi from Indonesia Climate Change Trust Fund (ICCTF) highlighted four main challenges for the blue carbon ecosystem in Indonesia:

- unavailability of blue carbon roadmap;

- lack of updated data for baseline and monitoring;

- blue carbon being less prioritized in Indonesia’s NDC; and

- the need to mainstream blue carbon policy into provincial/district level.

The need for partnerships

Partnerships can enhance blue carbon ecosystems by taking important measures such as policy influence, resource sharing, multistakeholder collaboration, community involvement, and monitoring and research. Currently, there are ten key Indonesian ministries/institutions in the policy-making process for blue carbon management, categorized into two different groups:

- coordination and policy;

- and technical implementation.

The Coordinating Ministry for Maritime and Investments Affairs (Kemenkomarves) holds the lead role of coordination amongst institutions.

Unclear ownership in the blue carbon ecosystem

The lively Q&A session included representatives from multiple sectors and backgrounds such as project developers, legal firms, CSOs, and government. Participants agreed that private sector involvement is critical for exploring the potential of blue carbon in Indonesia. Another issue raised was the unclear regulation of carbon ownership in the blue carbon ecosystem, especially for mangroves. A participant, who is part of project developers, shared his experience on the long and complex process of getting concession permits for forestry projects. This could even be worse for blue carbon due to the lower amount of attention it receives from the government, the participant added.

Addressing key challenges to unlock Indonesia’s Blue Carbon Potential

International communities have been eyeing the potential of nature-based carbon credits in Indonesia, including from blue carbon projects. However, participants agreed that blue carbon is still deemed as less of a priority for selling on the carbon market despite existing regulations such as PR 98/2021 and MOEF Reg 21/2022. Issues like unclear regulatory frameworks, lack of interministerial coordination, and long-winding administration processes would often signal investments away. If these issues aren’t addressed properly, it could threaten the attractiveness of blue carbon credits and discourage the whole “blue economy” vision for Indonesia.

Materials

Introduction to Blue Carbon

presented by Sarfina Adani, Consultant, Neyen

The Development of Blue Economy Framework at Sub-National Level: The Case Study Of West Java Province

presented by Eka Jatnika Sundana, Head of Economy & Natural Resources Division of Regional Development Planning Agency of West Java Province (Bappeda Jabar)

Supporting Government for Blue Carbon Management in Indonesia

presented by Amrullah Rosadi, Indonesia Climate Change Trust Fund (ICCTF)